Chargebacks are a daily headache for many US florists.

Margins are already tight, flowers are perishable, and deliveries are time-sensitive.

When a customer disputes a card payment and wins, you don’t just lose the sale — you lose the product, the time, the delivery cost, and then get hit with a chargeback fee on top of it.

In the floral industry, the same small group of issues tends to appear again and again: late deliveries, flowers “not as described,” substitution problems, billing confusion, and claims that an order was never placed or never received. Understanding common chargeback reasons in the floral industry — and how card networks classify them — is the first step to lowering your dispute rate, keeping your processing costs under control, and protecting your reputation.

This guide focuses on US florists (retail shops, studio florists, event florists, and online floral brands) and reflects the current Visa and Mastercard dispute framework used in 2024–2025.

What Are Chargebacks and Why They Matter to Florists

A chargeback is a forced reversal of a card transaction initiated by the cardholder’s bank (issuer). The customer contacts their bank instead of you, claims something went wrong with the order, and the bank pulls the funds back from your acquiring bank or payment processor. You lose the revenue unless you successfully contest the dispute with evidence that contradicts the customer’s claim.

Card networks like Visa and Mastercard use “reason codes” to classify each chargeback. For example, Visa groups its codes into four categories: fraud (10.x), authorization issues (11.x), processing errors (12.x), and consumer disputes (13.x).

Common codes that affect florists include 10.4 (Other Fraud – Card-Absent Environment), 13.1 (Merchandise/Services Not Received), 13.3 (Not as Described/Defective Merchandise), and 13.6 (Credit Not Processed).

Mastercard uses a different numbering scheme, but the themes are similar — for example, 4837 (No Cardholder Authorization) and 4853 (Services Not Provided or Merchandise Not Received).

For florists, the financial impact is bigger than just one lost sale. Each dispute can trigger:

- Lost cost of goods (flowers, vase, packaging, card, ribbon).

- Lost labor (design time, admin time, delivery time).

- Delivery and fuel costs you can’t recover.

- Processor chargeback fees and higher long-term processing rates.

- Risk of being flagged for card-network monitoring programs if your chargeback ratio exceeds thresholds.

Because floral sales spike around holidays like Valentine’s Day, Mother’s Day, graduations, and funerals, a small operational issue can suddenly create many chargebacks at once. That’s why understanding common chargeback reasons in the floral industry is essential: it lets you design systems, policies, and scripts that directly target the root causes of disputes.

Unique Risk Factors Behind Chargeback Reasons in the Floral Industry

The floral business has risk factors that most other retail categories never deal with. Flowers are perishable, highly seasonal, and emotionally charged — they’re purchased for weddings, funerals, apologies, anniversaries, and major holidays.

When something goes wrong, the customer feels it deeply, and a chargeback can feel like the easiest way to demand satisfaction.

Unlike standard e-commerce, floral orders are often:

- Time-specific (“arrive before 10 a.m. for the funeral”).

- Occasion-sensitive (Mother’s Day, Valentine’s Day, sympathy, hospital deliveries).

- Location-complex (churches, venues, hospitals with strict rules, cemeteries).

Add in third-party wire services, last-minute orders, and ever-changing flower availability, and you get a perfect storm for misunderstandings and disputes. Floral customers may interpret normal industry practices — such as substitutions when certain stems are unavailable — as bait-and-switch if they weren’t clearly explained ahead of time.

In this context, understanding common chargeback reasons in the floral industry means looking beyond generic fraud and “item not received” disputes, and paying attention to floral-specific risk factors: seasonal spikes, substitution policies, delivery window expectations, and the way your store coordinates with wire services and marketplace platforms.

Seasonality, Capacity, and Time-Sensitive Events

Seasonality and capacity constraints are major drivers of chargeback reasons in the floral industry. During Valentine’s Day, Mother’s Day, Christmas, and prom season, floral shops can be pushed far beyond their usual daily volume.

That’s when delivery delays, mixed-up orders, and missed time windows spike — and those issues map directly to “merchandise/services not received” chargebacks.

Customers often expect exact timing: funeral sprays before the service starts, wedding bouquets before photos, birthday deliveries during office hours, or surprise deliveries when the recipient is home. If your routing or capacity planning isn’t realistic, drivers get behind schedule.

A bouquet that arrives after the funeral or after the recipient has left the office may technically be “delivered,” but to the buyer it feels like a complete failure. That emotional disappointment frequently turns into disputes.

US florists also face weather-related constraints (extreme heat, snowstorms, hurricanes, wildfires). When roads close or flights are delayed, flowers may wilt in transit or arrive late.

If your confirmation emails and website don’t clearly state how you handle force majeure situations — and your team doesn’t proactively communicate delays — customers may bypass your customer service and ask their bank to reverse the charge.

To reduce seasonality-driven chargeback reasons in the floral industry, you need upstream fixes, not just better dispute responses: realistic holiday cut-off times, clear messaging about delivery windows, accurate inventory, and dynamic capacity controls that prevent over-booking on peak days.

Substitutions, Design Variations, and Expectation Gaps

Substitutions are normal in floral design. Due to seasonality, local availability, and last-minute supplier issues, florists often swap certain blooms, greenery, or containers while still trying to maintain overall style and value.

Industry programs like FTD’s substitution guidelines emphasize maintaining the design’s theme, color story, and value, and notifying the sending florist or customer when substantial substitutions are required.

However, customers ordering online may assume the product photo is an exact blueprint. When they see different flowers, fewer premium stems, or a different container, they may feel misled.

That disappointment is one of the most common chargeback reasons in the floral industry and often comes through as “Not as described or defective merchandise” (Visa 13.3) or similar cardholder dispute codes.

Expectation gaps also show up in:

- Color variations (e.g., “hot pink roses” that look more coral or red in real life).

- Bloom stage (tight buds vs fully open blooms).

- Perceived size (arrangements looking larger in photos than on the table).

- Longevity (customers expecting a week of freshness when stems naturally last 3–5 days).

If your product pages, substitution policies, and care instructions are vague, you invite claims that the arrangement was “wrong” or low quality. Over time, those disputes accumulate and become a measurable pattern when you analyze chargeback reasons in the floral industry.

Transparent substitution policies, clear product descriptions, real-world photography, and proactive communication about any major design changes are crucial defenses against this bucket of disputes.

Wire Services, Marketplaces, and “Who Is the Merchant?” Confusion

Many US florists work with wire services and marketplaces (such as FTD, Teleflora, and other national brands) that aggregate online orders and route them to local filling florists. While this can boost volume, it also complicates billing and dispute handling, which directly affects chargeback reasons in the floral industry.

The customer’s card is usually charged by the wire service, not the local florist. The descriptor on the statement shows the network brand, not your shop name.

If the customer is unhappy, they may not realize a local florist fulfilled the order at all. They file a chargeback against the brand they recognize, and the dispute is routed through the wire service’s process.

Additional risk arises from service fees, “junk fees,” and unexpected charges added late in the checkout flow. Recent litigation around hidden delivery fees in the floral sector shows how sensitive US regulators and consumers are to last-minute price changes.

If customers feel misled about fees, they’re more likely to dispute the entire charge, citing misrepresentation or not-as-described.

For independent shops that also run their own website, this can create a double layer of confusion: the same logo may appear via wire services and your direct site, but the billing descriptor, customer service process, and refund policies differ.

Clarifying who is charging the card, who is fulfilling the order, and who handles complaints is critical to reducing these confusion-driven chargeback reasons in the floral industry.

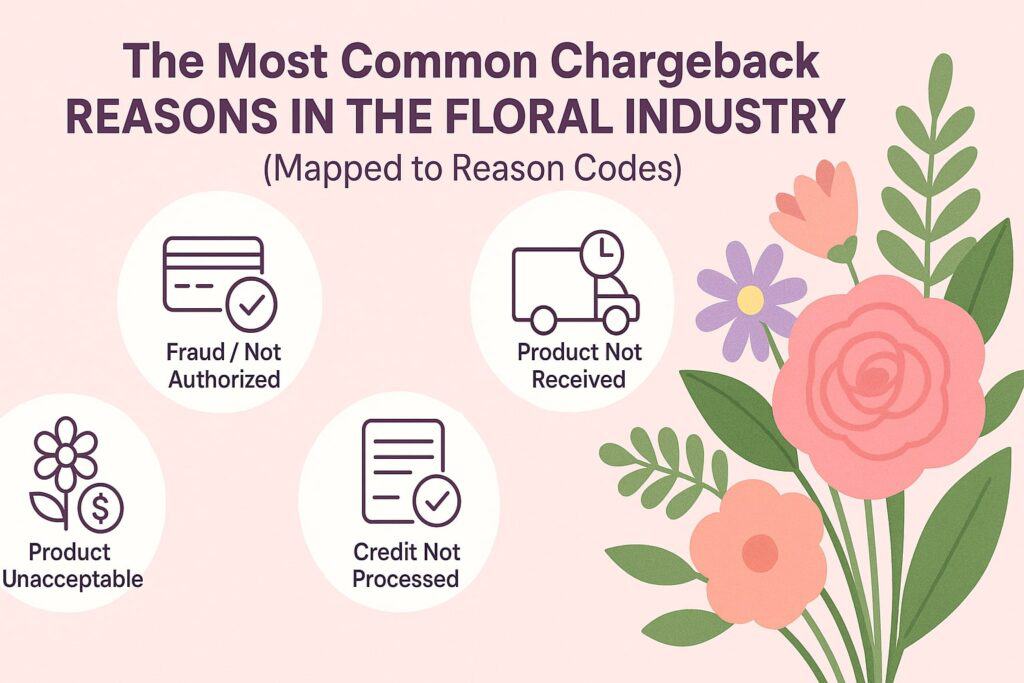

The Most Common Chargeback Reasons in the Floral Industry (Mapped to Reason Codes)

While every processor reports disputes a little differently, most data and industry experience show that the top chargeback reasons in the floral industry fall into four main buckets:

- Merchandise/services not received (delivery problems).

- Not as described or defective (quality/design problems).

- Fraud/unauthorized transactions (true and friendly fraud).

- Processing and refund issues (duplicate charges, incorrect amounts, credit not processed).

These map cleanly to card-network reason codes that your acquirer or payment processor will show on the chargeback notice. Understanding those mappings helps you quickly identify root causes, refine your processes, and prepare targeted evidence when you fight disputes.

“Merchandise or Services Not Received” – Late, Missed, or Misrouted Deliveries

For florists, “Merchandise/Services Not Received” is one of the most frequent chargeback reasons. On the Visa side, this is typically Reason Code 13.1 (Merchandise/Services Not Received). Mastercard’s equivalent often appears as 4853 (Services Not Provided or Merchandise Not Received).

In the floral context, customers may claim:

- The order never arrived at the address.

- It arrived after the event (e.g., funeral, wedding, birthday).

- It was left in the wrong place (wrong apartment, lobby, neighbor’s porch).

- It was delivered but was already wilted or damaged and might as well have been “not received.”

Sometimes these disputes are valid: a driver missed the address, a routing error occurred, or an order was sent out on the wrong day. But in many cases, the flowers were delivered — just not noticed, not brought inside, signed for by someone else, or stolen after delivery.

“Order not received” is also a common pretext for friendly fraud, where a customer uses the banking system like an unofficial refund channel even though they got what they ordered.

To fight these chargeback reasons in the floral industry, your best evidence includes:

- Detailed delivery logs (date, time, GPS coordinates if available).

- Signed delivery slips or photos showing the order at the door or with the recipient.

- Driver notes (who accepted delivery, where it was left, any access issues).

- Communications where the customer confirmed receipt or thanked you.

Prevention starts with clear delivery windows, accurate address verification, driver training, and proof-of-delivery tools (photos, signatures, geotagging) that are standard in many modern delivery apps.

“Not as Described or Defective” – Quality, Freshness, and Design Disputes

Another core set of chargeback reasons in the floral industry falls under “Not as Described/Defective Merchandise,” which Visa categorizes as Reason Code 13.3.

Typical floral complaints include:

- “The bouquet looks nothing like the photo.”

- “They used cheap filler instead of the premium blooms I ordered.”

- “The flowers arrived brown, crushed, or already dying.”

- “The arrangement was much smaller than shown online.”

These disputes often arise from a combination of legitimate issues (poor quality control, mishandling in transit, incorrect recipes) and expectation gaps (substitutions that weren’t explained, product photos shot at flattering angles, differences in bloom stages).

Industry substitution guidelines stress that when a florist must substitute, they should maintain style, color scheme, and value, and notify the sending florist or customer when possible — but not every shop follows this rigorously.

To prevent “not as described” chargebacks in the floral industry, focus on:

- Clear, honest product photos and descriptions that show realistic sizes.

- Specific substitution language on product pages and in order confirmations.

- Internal recipe controls so designers know the stem count and premium elements.

- Quality checks at dispatch (no bruised petals, clean vases, untangled ribbons).

- Care instruction cards and tips to maximize vase life.

When you do face these disputes, valuable evidence includes delivery photos, internal recipes showing equivalent value, customer service tickets showing you offered a replacement, and your published substitution and quality policies that the customer agreed to at checkout.

Unauthorized/Fraudulent Transactions – Online Floral Scams and Friendly Fraud

Unauthorized transaction chargebacks are labeled as fraud by the card networks. For Visa, one of the most common e-commerce fraud codes is 10.4 (Other Fraud – Card-Absent Environment). For Mastercard, a similar “no cardholder authorization” scenario is 4837.

In the floral world, fraud can show up in several ways:

- Stolen card details used to place large or last-minute orders, often for high-value arrangements, add-ons, or gift baskets.

- Orders shipping to addresses unrelated to the cardholder, sometimes international freight forwarders, vacant properties, or short-term rentals.

- Friendly fraud, where the cardholder (or a family member) legitimately placed the order, but later denies it to their bank.

Seasonal spikes around Mother’s Day and Valentine’s Day are also prime time for phony florist websites and scam ads. The BBB routinely warns US consumers about fake florist sites that take payments and never deliver, which leads to legitimate chargebacks when customers get nothing at all.

Those same heightened fraud patterns can spill over onto real florists, as banks become more suspicious of floral transactions during peak seasons.

To defend against these fraud-related chargeback reasons in the floral industry, you should:

- Use AVS (Address Verification Service), CVV checks, and 3-D Secure or network tokenization where available.

- Flag orders with mismatched billing and delivery addresses, disposable emails, or international IP addresses.

- Set rules for manual review of high-risk orders (high dollar, rush orders, unusual locations).

- Maintain clear, consistent billing descriptors so customers recognize your name on their statements.

When a fraud dispute hits, evidence of proper authorization (AVS and CVV match, 3-D Secure authentication, IP logs, device fingerprints, proof of delivery) can help you contest friendly fraud, even though true fraud is rarely recoverable.

Duplicate, Incorrect Amount, or Processing Errors

Not all chargeback reasons in the floral industry are emotional or fraud-related. Some are pure processing mistakes. Visa’s 12.x series covers processing errors such as incorrect amount, wrong currency, duplicate processing, and invalid data. Mastercard has comparable codes, including 4808 (authorization/processing errors).

Common floral scenarios include:

- Accidentally charging the card twice when the terminal freezes or the online page is refreshed.

- Charging the wrong amount (forgetting a discount, mis-keying a tip, adding or omitting tax).

- Re-submitting an offline transaction after it was already captured.

- Charging in the wrong currency for cross-border orders.

From the customer’s point of view, these are straightforward errors. They either paid too much or saw duplicate charges. If customer service is slow or unhelpful, they’ll go straight to the bank, and you’ll see a cluster of processing-error disputes.

Prevention is mostly operational: training staff, using integrated POS and e-commerce systems, reconciling batches daily, and putting simple controls in place (like mandatory manager approval for manual key-ins or adjustments over a certain amount).

When these chargebacks do occur, you often can’t win them — the error is real — but you can avoid repeat issues by tightening your workflows.

Credit Not Processed and Cancellation Disputes

“Credit Not Processed” and “Cancelled Merchandise/Services” are another major cluster of chargeback reasons in the floral industry. Visa uses codes like 13.6 (Credit Not Processed) and 13.7 (Cancelled Merchandise/Services), and similar themes appear in other networks.

These disputes typically happen when:

- You promised a refund or partial credit but never issued it, or it was delayed beyond the customer’s expectations.

- The customer cancels an order before your stated cut-off, but your team fails to stop production and charges them anyway.

- Your cancellation policy is unclear, hidden, or appears unfair (e.g., “no cancellations” even days in advance).

- The customer is told “store credit only” when the law or your own terms call for a refund to the original payment method.

Florists often try to protect themselves by using strict policies for same-day delivery, holidays, or custom event work. However, if those policies aren’t clearly shown on product pages, in the cart, and in the confirmation email, customers may feel blindsided.

That confusion is a major driver of chargeback reasons in the floral industry related to credits and cancellations.

To reduce this category:

- Make your cancellation and refund policy prominent, plain-language, and consistent across your website, receipts, and in-store signage.

- Automate refund flows in your POS and gateway so staff can’t forget to process agreed credits.

- Use email templates that confirm “We have cancelled your order and your refund of $X has been issued; you should see it on your statement within Y business days.”

How to Prevent the Most Common Chargeback Reasons in the Floral Industry

Once you know the main chargeback reasons in the floral industry, prevention becomes a matter of designing your customer journey, operations, and payment flows around those risks. Every step — from product page to delivery photo — should either set the right expectation or document that you delivered what was promised.

Strengthening Product Pages, Order Capture, and Substitution Policies

Your website and phone scripts are your first line of defense. Many chargeback reasons in the floral industry — especially “not as described” and “misrepresentation” claims — stem from vague product descriptions and buried policies.

Borrowing from best practices used by established US florists, you should:

- Use realistic photography: Show arrangements at actual scale (e.g., next to a chair, on a dining table). Avoid overly stylized images that create unrealistic expectations of size or fullness.

- Describe size and recipe clearly: Use simple tiers like “standard, deluxe, premium” and explain what changes at each level (more stems, larger container, more premium blooms).

- Publish a clear substitution policy: State when substitutions may occur, how you maintain value and style, and when you will call the customer before making major changes. Model your policy on professional guidelines (like FTD’s) that stress style, color, and value equivalence.

- Highlight time-sensitive details. For funerals, hospital deliveries, schools, and workplaces, explain cut-off times and what “same-day” really means in your zip codes.

- Collect complete delivery details. Require building names, suite numbers, gate codes, contact phone numbers, and any special instructions.

On phone orders, train staff read back key details (“So we’re doing the deluxe ‘Spring Garden’ arrangement with an ‘as similar as possible’ substitution if tulips aren’t available…”) and note that in the ticket. That way, if a dispute arises, you can show that the customer explicitly agreed to the design and substitution approach.

Delivery Operations, Proof of Delivery, and Communication

Because so many chargeback reasons in the floral industry center on delivery complaints, your logistics and communication strategy matter as much as your design skills.

Key practices include:

- Proof of Delivery (POD). Train drivers to capture photos of deliveries at the door or with the recipient, plus signatures where appropriate. Log date, time, and any notable circumstances (“left with receptionist Mary at front desk”).

- Realistic delivery windows and cut-offs. Don’t promise “same-day delivery by 3 p.m.” if your zip-code coverage and staff can’t support it at peak times. Adjust cut-offs for major holidays and advertise them early.

- Proactive communication. Text or email customers when the order is on its way and when it’s delivered. If you foresee a delay, notify them before the disappointment hits.

- Clear policy for re-delivery. For failed deliveries (closed business, incorrect address, recipient not home), clearly state whether you will attempt re-delivery, leave the order, or charge a re-delivery fee — and communicate this upfront at checkout.

- Weather and force-majeure messaging. When storms, extreme heat, or wildfires impact routes, update your homepage and send bulk emails explaining the situation, how it affects timing, and what flexibility you’re offering.

The more documentation you have around delivery, the easier it is to dispute “not received” claims and reduce this large share of chargeback reasons in the floral industry.

Fraud Prevention, Billing Descriptors, and Online Checkout Practices

A modern fraud strategy is essential for any US florist with online ordering. Fraud-related chargeback reasons in the floral industry are costly because they combine lost product, lost revenue, and high chargeback-monitoring risk.

Best practices include:

- Use basic fraud tools: Turn on AVS, CVV, and 3-D Secure or network-specific tools offered by your processor.

- Set risk rules: Flag orders where billing and delivery countries differ, IP geolocation doesn’t match the billing region, or the email domain is disposable.

- Limit high-risk behaviors: Require additional verification for unusually large orders, urgent same-day orders to unfamiliar addresses, or multiple card attempts from the same device.

- Optimize your billing descriptor: Make sure the name that appears on statements clearly matches your brand (“Rose Lane Florist, City ST”) and avoid obscure corporate names that customers won’t recognize. Many “fraud” disputes are really “I didn’t recognize this charge” disputes.

- Store customer history: Frequent repeat customers with consistent behavior can be treated as lower-risk, while new customers with high-risk patterns warrant extra review.

By aligning your checkout and billing practices with card-network guidance, you directly reduce fraud-related chargeback reasons in the floral industry and improve your win rate on disputes that are actually friendly fraud.

Customer Service, Refund Flows, and Root-Cause Analysis

Many chargebacks happen only because customers feel ignored or stuck. Good customer service can intercept a large percentage of disputes before they reach the bank, especially when the customer’s issue is quality, delivery timing, or minor billing confusion.

Practical steps:

- Multiple contact channels: Offer phone, email, and chat or SMS support, especially around holidays. Make these contact options prominent in emails and on receipts.

- Fast response SLAs: Aim to respond to complaints within a few business hours, not days. Delays increase the likelihood of a chargeback.

- Empower staff to resolve issues: Give your team clear rules for when to offer a redelivery, partial refund, or full refund. Empowerment reduces escalations.

- Automated refunds: Use integrated POS and gateway tools so staff can issue card refunds quickly and correctly, reducing “credit not processed” disputes.

- Regular root-cause reviews: Categorize disputes by reason code and internal cause (e.g., “delivery late – capacity issue,” “substitution misunderstood,” “duplicate processing”) and review them monthly.

By treating every dispute as a data point, you turn chargeback reasons in the floral industry into an internal feedback loop that makes your shop stronger and more resilient.

Responding to Chargebacks: Step-by-Step Playbook for US Florists

Even the best-run floral shop will still see some disputes. When a chargeback hits, how you respond determines whether you recover the funds and how card networks view your risk profile.

Reading the Chargeback Notice and Reason Code

When you receive a chargeback notification from your processor or acquiring bank, it will include:

- The transaction details (date, amount, last four digits of the card).

- The reason code, which is your clue to cardholder claims and required evidence.

- A reply-by date, by which you must submit evidence or accept the loss.

Your first step is to map that code to a real-world scenario in your shop. For example:

- Visa 13.1 – customer says “flowers never arrived.”

- Visa 13.3 – customer says “arrangement not as described or defective.”

- Visa 10.4 – customer says “I didn’t authorize this online order.”

- Mastercard 4837 – customer says “I never approved this charge.”

Once you understand the category of chargeback reasons in the floral industry that this dispute fits into, you can decide whether it’s worth fighting and what documents you need.

Building Compelling Evidence Packages for Floral Transactions

Card networks require “compelling evidence” to overturn a chargeback — not just your word against the customer’s. The type of evidence you submit should match the reason code and the specific chargeback reasons in the floral industry you’re dealing with.

Examples:

- For “not received” disputes (13.1 / 4853):

- Delivery logs with timestamps.

- GPS data or route records.

- Delivery photos at the door or with the recipient.

- Signed slips or internal notes (“left with receptionist”).

- Email or SMS confirming delivery or thanks from the buyer/recipient.

- Delivery logs with timestamps.

- For “not as described/defective” disputes (13.3):

- Product page screenshot and substitution policy as of order date.

- Internal recipe or recipe card showing stem counts and value.

- Photos taken immediately after design and at delivery.

- Customer communications showing that you offered a replacement or refund and their response.

- Product page screenshot and substitution policy as of order date.

- For fraud/unauthorized disputes (10.4 / 4837):

- AVS and CVV match results.

- 3-D Secure authentication results or tokenized authorization details.

- IP address and device fingerprint.

- Proof of delivery, especially when shipping to the cardholder’s address.

- AVS and CVV match results.

- For credit/cancellation disputes (13.6 / 13.7):

- Copy of your refund and cancellation policy.

- Screenshots showing where it appears during checkout.

- Refund logs from your gateway or POS.

- Emails confirming cancellation, or showing customers cancelled after cut-off.

- Copy of your refund and cancellation policy.

Organize evidence clearly, label each document, and include a short narrative that connects the dots in plain language. Processors and issuers handle thousands of disputes; clarity improves your odds of winning.

When to Fight vs. When to Accept and Learn

Not every dispute is worth fighting. A key part of managing chargeback reasons in the floral industry is strategic triage.

You may decide to accept a chargeback when:

- The order clearly failed (missed funeral, wrong product, poor quality).

- The amount is small and evidence is weak or missing.

- The cost of staff time and documentation exceeds the likely benefit.

You should strongly consider fighting a chargeback when:

- You have clear proof of delivery and customer acknowledgment.

- The order value is high (weddings, large sympathy pieces, event installations).

- You suspect friendly fraud and want to discourage repeat behavior.

Regardless of the outcome, log each dispute in your internal system by root cause. Over time, you’ll see patterns — specific drivers, delivery zones, products, or holidays that generate a disproportionate share of chargeback reasons in the floral industry for your shop.

Building a Long-Term Chargeback Strategy in a Floral Business

Prevention and response are important, but long-term success comes from treating chargebacks as a measurable business metric, just like conversion rate or cost of goods.

Key elements of a sustainable strategy:

- Track your chargeback ratio: Measure chargebacks as a percentage of monthly Visa and Mastercard sales. Card networks monitor this ratio, and high levels can lead to fines or placement in monitoring programs.

- Segment by reason and product type: Break disputes into categories — delivery, quality, processing error, fraud. Look for patterns in specific SKUs (e.g., certain designs or add-ons) or service types (funerals, weddings, online orders).

- Review policies at least annually: As card-network rules and US consumer expectations change, adjust your substitution policy, cut-off windows, and refund terms.

- Train staff regularly: Front-line staff should understand why chargebacks matter, how to de-escalate complaints before they reach the bank, and how to document orders and deliveries.

- Work with your payment partner: A knowledgeable merchant services provider can help you interpret reason-code trends, set up fraud tools, and monitor your dispute metrics over time.

By aligning your systems with how card networks actually categorize chargeback reasons in the floral industry, you move from reactive firefighting to proactive risk management.

FAQs

Q1. What are the most common chargeback reasons for US florists?

Answer: The most common chargeback reasons in the floral industry are:

- Merchandise/services not received (missed or late deliveries).

- Not as described/defective (substitutions, quality, size issues).

- Unauthorized transactions (fraud and friendly fraud).

- Credit not processed or cancellation disputes.

These map to Visa codes like 13.1, 13.3, 13.6, 13.7, and 10.4, and Mastercard codes like 4837 and 4853.

Q2. How long do customers have to file a chargeback on a flower order?

Answer: Time limits vary by card network and sometimes by specific reason code, but generally cardholders have up to about 120 days from the transaction or from when they expected to receive the flowers for most consumer-dispute codes (like not received or not as described).

Merchants typically have a shorter window — often 30–45 days — to respond with evidence once a chargeback is filed.

Check your processor’s documentation and the latest Visa and Mastercard rules to confirm exact timelines, as they can change.

Q3. Are substitutions a valid defense against ‘not as described’ disputes?

Answer: Substitutions can be a valid defense if you can show that:

- Your substitution policy was clearly disclosed at the time of order.

- The arrangement delivered was reasonably similar in style, color, and value.

- Substitutions were necessary due to seasonal or local availability, not cost-cutting.

Including before-delivery photos, internal recipes, and your published substitution policy in your evidence package significantly improves your chances of overturning “not as described” chargeback reasons in the floral industry.

Q4. How can I reduce fraud and unauthorized chargebacks for online floral orders?

Answer: To reduce fraud-related chargeback reasons in the floral industry, you should:

- Enable AVS and CVV checks, and consider 3-D Secure where supported.

- Use fraud-screening tools that flag high-risk orders (large amounts, mismatched addresses, suspicious IPs).

- Maintain a clear, recognizable billing descriptor that matches your trading name.

- Manually review risky orders, especially during major US flower holidays.

Q5. What’s the best way to handle complaints so they don’t turn into chargebacks?

Answer: Respond quickly, listen carefully, and empower your team to offer fair solutions. Many chargeback reasons in the floral industry stem from customers feeling ignored or dismissed.

Provide easy ways to contact you, acknowledge the issue, and offer remedies such as redelivery, partial refunds, or credit when appropriate. Quick, empathetic responses often keep disputes out of the banking system altogether.

Conclusion

Understanding common chargeback reasons in the floral industry isn’t just about avoiding fees — it’s about building a more reliable, customer-centric floral business. Disputes highlight weak spots in your photos, policies, delivery operations, fraud controls, and customer service.

By mapping each dispute to a real-world cause, aligning your policies with card-network rules, and documenting every step of your process, you can:

- Reduce how often customers feel the need to go to their bank.

- Improve your win rate when disputes do occur.

- Keep your chargeback ratio below monitoring thresholds.

- Build trust with customers who know you’ll stand behind your work.

In a US floral market where online ordering, wire services, and instant reviews shape buying behavior, turning chargeback reasons in the floral industry into a source of insight — rather than just frustration — can become one of your strongest competitive advantages.